The PROBPORT Test

Problems

Contributed by:

Feng Qiu

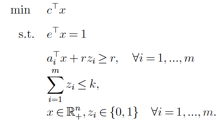

The probport test problem suite consists of 20 instances of a chance constrained portfolio optimization problem of the form:

The continuous variables represent investment in n assets, the coefficient vector a_i represent the return of the assets under scenario i, and cost vector c represent the investment cost, and r is the required return. The vector e is a vector of ones. The investment should be such that the portfolio return exceeds the required return r in at least m-k of the m scenarios.

The instances are grouped into two sets of 10 instance each: probport and probport_nr. The instances in the first group include a budget constraint (the first constraint shown above) and while those in the second group do not. Each instance has n=20, m=200, k=15. The instances are provided in mps format. Details on the generation of the instance data and associated computational results is available in [1].

REFERENCE:

[1] Feng Qiu, Shabbir Ahmed, Santanu S. Dey and Lawrence Wolsey. Covering Linear Programming with Violations. To appear in INFORMS J. on Computing, 2013.